Learn how to do anything. The world's most popular how-to website

Home

› Journalizing Closing Entries : Solved: Journalize The Closing Entries. Include Posting Re ... : An income summary account is used to summarize revenue and expense accounts, and establishing the net profit or loss for the period.

Journalizing Closing Entries : Solved: Journalize The Closing Entries. Include Posting Re ... : An income summary account is used to summarize revenue and expense accounts, and establishing the net profit or loss for the period.

Journalizing Closing Entries : Solved: Journalize The Closing Entries. Include Posting Re ... : An income summary account is used to summarize revenue and expense accounts, and establishing the net profit or loss for the period.. It involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet. Companies use closing entries to reset the balances of temporary accounts − accounts that show balances over a single accounting period − to zero. We were first introduced to closing journal entries in chapter 6. 31 fees income 401 35,000.00 income summary 309 35,000.00 31 income summary 309 12,367.00 Summary of closing entries general journal page 4 post.

In addition, any transaction that increases or decreases capital should also be posted to the appropriate capital account. At the month end a business needs to be able to calculate how much profit it has made. 31 fees income 401 35,000.00 income summary 309 35,000.00 31 income summary 309 12,367.00 Closing entries are based on the account balances in an adjusted trial balance. Select the explanation on the last line of the journal entry table.) start by closing revenues.

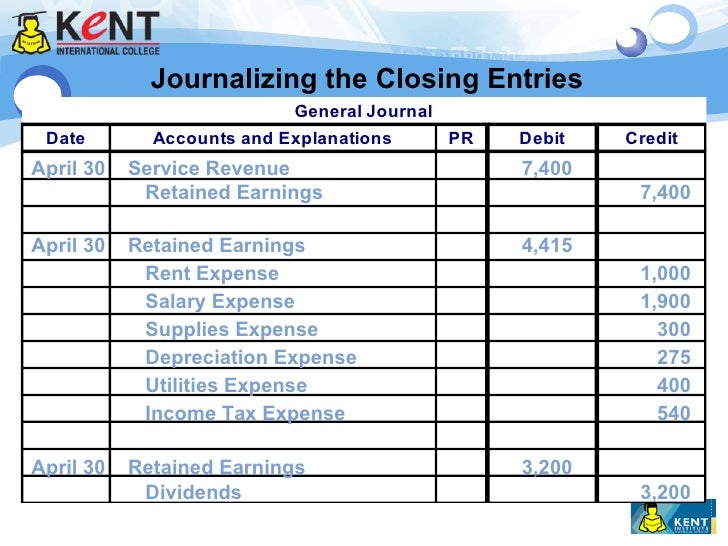

CHSS Principles of Accounts for CSEC : General Journal ... from www.cliffsnotes.com The closing entries are the journal entry form of the statement of retained earnings. Journalize the closing entries at april 30. A closing entry is a journal entry made at the end of the accounting period. This resets the balance of the temporary accounts to zero, ready to begin the next accounting period. In other words, temporary accounts are reset for the recording of transactions for the next accounting period. Closing entries take place at the end of an accounting cycle as a set of journal entries. This is done by journalizing those entries in the general journal and then posting them to the general ledger. Closing journal entries are used at the end of the accounting cycle to close the temporary accounts for the accounting period, and transfer the balances to the retained earnings account.

S4 9 journalizing closing entries brett tamas enterprises had the following from acct 2301 at university of texas

Closing journal entries are used at the end of the accounting cycle to close the temporary accounts for the accounting period, and transfer the balances to the retained earnings account. This is accomplished by journalizing and posting closing entries for all temporary accounts. Journalizing and posting closing entries the eighth step in the accounting cycle is preparing closing entries, which includes journalizing and posting the entries to the ledger. Your closing journal entries serve as a way to zero out temporary accounts such as revenue and expenses, ensuring that you begin each new accounting period properly. A closing entry is a journal entry that is made at the end of an accounting period to transfer balances from a temporary account to a permanent account. Closing entries closing entries are manual journal entries at the end of an accounting cycle to close out all the temporary accounts and shift their balances to permanent accounts. (record debits first, then credits. As part of the procedure, a company will record journal entries that transfer all account balances from its income statement to the balance sheet, leaving all income and expense accounts with a. Closing entries, also called closing journal entries, are entries made at the end of an accounting period to zero out all temporary accounts and transfer their balances to permanent accounts. It involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet. Preparation of adjusting journal entries is the next step in the accounting cycle. Select the explanation on the last line of the journal entry table.) start by closing revenues. Closing entries take place at the end of an accounting cycle as a set of journal entries.

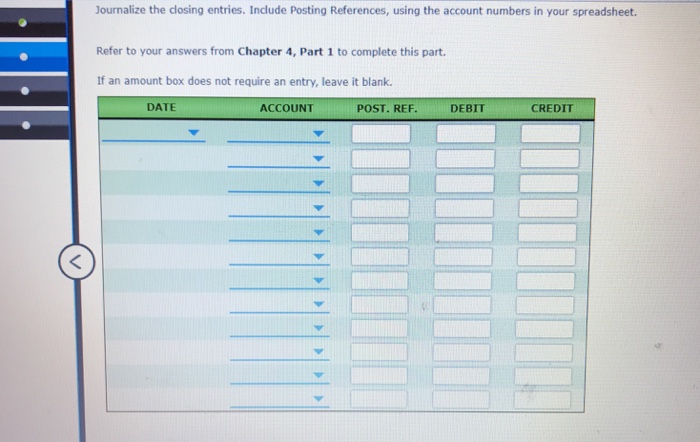

Journalize the closing entries for boston irrigation system. (record debits first, then credits. Closing entries, also called closing journal entries, are entries made at the end of an accounting period to zero out all temporary accounts and transfer their balances to permanent accounts. A closing entry is a journal entry made at the end of the accounting period. Ending inventory and cost of goods sold.

Chapter 3 add depreciation, closing entries, 4 diff ... from image.slidesharecdn.com Post the closing entries to income summary and retained earnings. This is done by journalizing those entries in the general journal and then posting them to the general ledger. Debit credit 2010 closing entries dec. Select the explanation on the last line of the journal entry table.) start by closing revenues. Examples of temporary accounts are the revenue, expense, and dividends paid accounts. A temporary account is an income statement account, dividend account or drawings account.it is temporary because it lasts only for the accounting period. Closing journal entries are used at the end of the accounting cycle to close the temporary accounts for the accounting period, and transfer the balances to the retained earnings account. Closing entries closing entries are manual journal entries at the end of an accounting cycle to close out all the temporary accounts and shift their balances to permanent accounts.

Closing entries are those journal entries made in a manual accounting system at the end of an accounting period to shift the balances in temporary accounts to permanent accounts.

Four entries occur during the closing process. In other words, the temporary accounts are closed or reset at the end of the year. Closing entries are based on the account balances in an adjusted trial balance. Preparation of adjusting journal entries is the next step in the accounting cycle. Post the closing entries to income summary and retained earnings. In accounting terms, these journal entries are termed as closing entries. A temporary account is an income statement account, dividend account or drawings account.it is temporary because it lasts only for the accounting period. At the month end a business needs to be able to calculate how much profit it has made. Closing entries are those journal entries made in a manual accounting system at the end of an accounting period to shift the balances in temporary accounts to permanent accounts. Closing entries, also called closing journal entries, are entries made at the end of an accounting period to zero out all temporary accounts and transfer their balances to permanent accounts. Companies use closing entries to reset the balances of temporary accounts − accounts that show balances over a single accounting period − to zero. Closing entries closing entries are manual journal entries at the end of an accounting cycle to close out all the temporary accounts and shift their balances to permanent accounts. Closing entries take place at the end of an accounting cycle as a set of journal entries.

As part of the procedure, a company will record journal entries that transfer all account balances from its income statement to the balance sheet, leaving all income and expense accounts with a. Journalizing closing entries for a merchandising enterprise at this point in the accounting cycle, we have prepared the financial statements. Select the explanation on the last line of the journal entry table.) start by closing revenues. This is commonly referred to as closing the books. 31 fees income 401 35,000.00 income summary 309 35,000.00 31 income summary 309 12,367.00

Solved: Journalize The Closing Entries. Include Posting Re ... from media.cheggcdn.com This resets the balance of the temporary accounts to zero, ready to begin the next accounting period. An income summary account is used to summarize revenue and expense accounts, and establishing the net profit or loss for the period. This video discusses how to journalize the closing entries into a general journal. Temporary accounts include the following: This is commonly referred to as closing the books. Closing entries take place at the end of an accounting cycle as a set of journal entries. Journalize the closing entries at april 30. Journalize the closing entries for boston irrigation system.

Overview of journalizing and posting closing entries closing entries are the journal entries that are recorded and posted to their respective ledger account in the ledger after the financial statement is completed.

Journalizing and posting the closing entries at the end of the period, the temporary accounts are closed. Closing entries, also called closing journal entries, are entries made at the end of an accounting period to zero out all temporary accounts and transfer their balances to permanent accounts. The videos in the adjusting entry section gave you a preview into this process but we will discuss it in more detail. Post the closing entries to income summary and retained earnings. An income summary account is used to summarize revenue and expense accounts, and establishing the net profit or loss for the period. As part of the procedure, a company will record journal entries that transfer all account balances from its income statement to the balance sheet, leaving all income and expense accounts with a. Closing entries are those journal entries made in a manual accounting system at the end of an accounting period to shift the balances in temporary accounts to permanent accounts. In addition, any transaction that increases or decreases capital should also be posted to the appropriate capital account. Closing journal entries are used at the end of the accounting cycle to close the temporary accounts for the accounting period, and transfer the balances to the retained earnings account. Closing journal entries are made at the end of an accounting period to prepare temporary accounts for the next period. Journalizing closing entries for a merchandising enterprise at this point in the accounting cycle, we have prepared the financial statements. Adjusting entries are entries made at the end of accounting period to bring all accounts up to date on an accrual accounting basis so that correct financial statements can be prepared. Closing entries may be defined as journal entries made at the end of an accounting period to transfer the balances of various temporary ledger accounts to some permanent ledger account.